Multi-Strategy Quant Systems - Algorithmic Trading In Python (Update)

Multi-Strategy Quant Systems - Algorithmic Trading In Python

Last updated 2/2022

MP4 | Video: h264, 1280x720 | Audio: AAC, 44.1 KHz

Language: English | Size: 4.12 GB | Duration: 6h 58m

Program in Python an End-to-End trading system from data management to order execution and risk management.

What you'll learn

Implement Multi-Strategy Quantitative Portfolios with Python

Build Modular Trading System such that components can be altered to trading preferences

Implement code for data pipelines, alpha research, alpha strats, portfolio allocation and order submission

Integrate with multiple brokerages with a single code base

Handle multiple alpha signals to create unified signals, and learn industry standard risk management techniques

Requirements

Basic Financial/Quantitative Literacy is expected.

Programming methodology (not necessarily in Python) is expected for coding in Python.

Ability to self-learn and comprehend documentation and code is expected.

Knowledge of tech stacks are NOT expected, basic software will be used.

Description

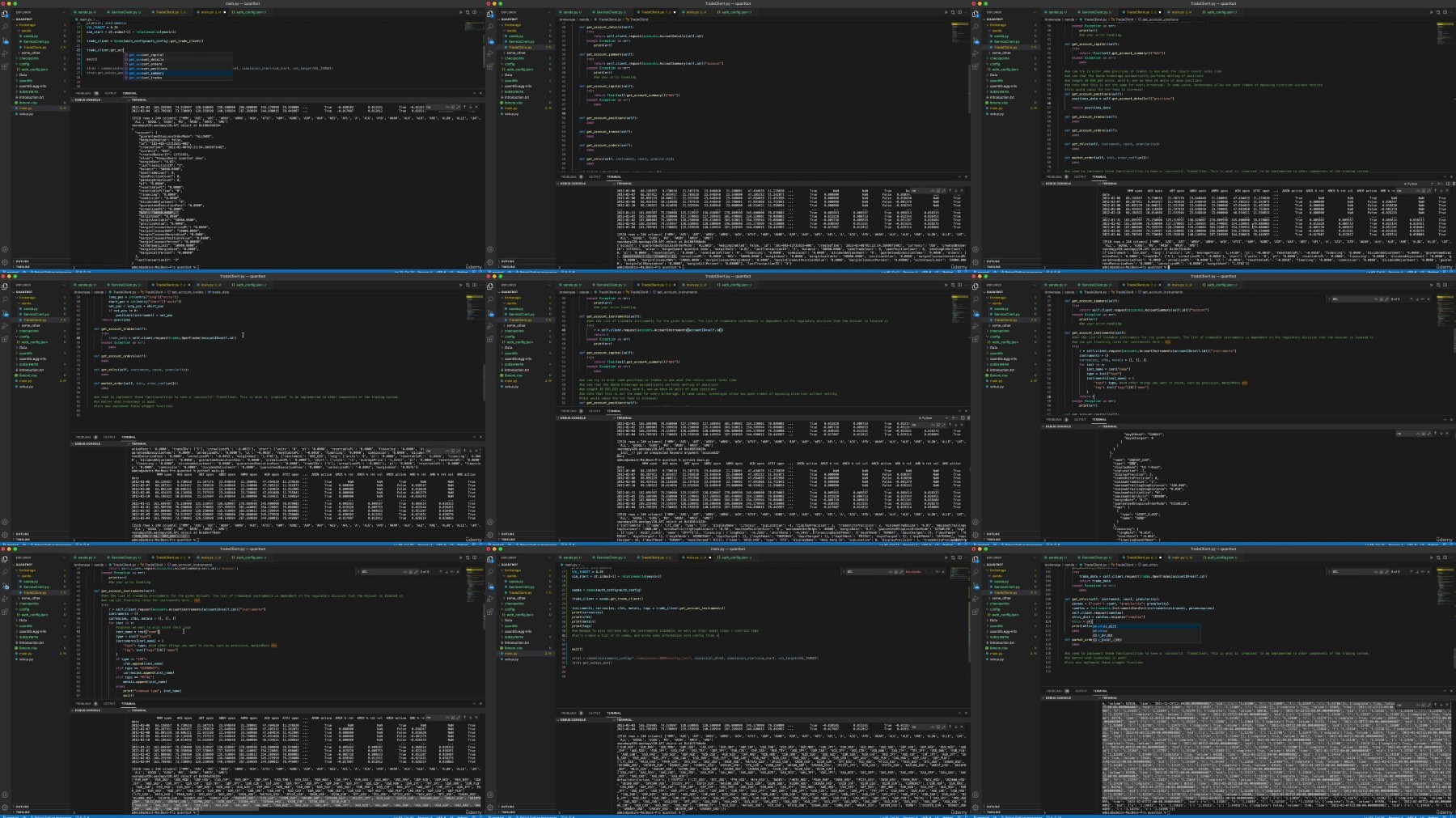

Multi-Strategy Quant Systems in Python from Scratch - A First Course in Algorithmic Trading by HangukQuant.As this is not a Python tutorial, we get right down to business and adopt a no-nonsense coding approach. It is advised that you slow down the pace of the course to your own needs. Even though only 7 hours of lectures have been distilled, the material within is fairly heavy. It is a walkthrough without the introductory explanations - since there are no explanations within the lecture walkthroughs, all students are expected to be hands-on and actively participate by asking questions; which we will compile in the Questions Section. Code is downloadable in Checkpoint Lectures.Watch a (sped-up) live recording of a quant implementing a shoestring trading system for non-HFT in Python, from data pipelines to order management. Build robust and flexible modular systems + take home a professional setup to adapt and improve.HangukQuant is the author of the 2nd highest rated quant trading blogs on Substack - Mathematics, Finance and Their Babies, with many years of experience in both quant research teams in both the industry and in academia.Implement a Multi Strategy Quantitative System in Python from Scratch, while learning how to build robust frameworks for implementation of alpha signals and capital allocation. Learn industry standards in risk management, such as volatility targeting schemes and technical diversification. Code along an algorithmic trading system with modular approaches to integrate with multiple brokerages and switch between them in a matter of seconds, all with the same code.Build diagnostic tools to analyse your trading system.Integrate with multiple brokerages in a single code base.Learn industry standards in risk management, such as volatility targeting schemes and technical diversification.Take back with you the final product - Your Very Own, Robust Quant Systems to hone and develop!Build quantitative strategies implementing factor premia and be given guidance for serious students of the market.This course is not a beginner course; financial literacy, and programming methodology is expected. Students are expected to be able to understand code without being prompted, or at least learn how to comprehend medium-sized code systems of thousands of lines of code. The course was first recorded and then sped up and voiced over chosen sections to meet Udemy course requirements. You may also choose to code along without the audio as the textual explanations should be primarily useful. As the course is an Advanced-Intermediate level, do note that you may face some difficulties along the way. It is expected that you would need to rewatch some of the lectures, and please do ask away in the Questions Section.Those without programming experience are encouraged to first undergo courses in Python / Programming Methodology / Data Science for Finance courses.Note that this course is not part of the Udemy Deals program, and no Udemy promotions are available. We believe that the material within is highly valuable and the cost price is cost de minimis in your quant journey.

Overview

Section 1: Introduction

Lecture 1 Introduction

Lecture 2 Obtaining S&P Tickers

Lecture 3 Obtaining the S&P Dataset

Lecture 4 Filling Missing Data and Supplementing Statistics

Lecture 5 Utility Functions and Pickling Data

Lecture 6 Developing Your Own Private Code Library

Section 2: Designing Flexible and Robust Quantitative Systems

Lecture 7 System Architecture and Version Tracking

Lecture 8 Implementing the Strategy API

Lecture 9 A Calculator For Indicators

Lecture 10 CHECKPOINT 1; Connecting The Strategy To Our Driver

Section 3: Strategy Implementation; Getting Alpha Signals

Lecture 11 LBMOM Strategy, Vol Targeting and Voting Systems

Lecture 12 CHECKPOINT 2; Calculating PnL, Strat Vol and Debugging

Section 4: Brokerage Implementation; Oanda

Lecture 13 Integrating with Oanda. Writing Wrapper Classes for the Oanda REST API

Lecture 14 CHECKPOINT 3; Implementing the Wrapper Functions and Getting Oanda OHLCV

Lecture 15 Writing Oanda Config Files

Lecture 16 CHECKPOINT 4; Implementing the Oanda Database Pipeline

Section 5: Working with FX and Non-USD Contracts

Lecture 17 Adding FX Information to the Data

Lecture 18 Writing a Master Config File

Lecture 19 CHECKPOINT 5; Implementing an FX Calculator

Section 6: Adding Multi Strategies

Lecture 20 Integration, Refactoring and Debugging

Lecture 21 CHECKPOINT 6; Implementing the LSMOM Strategy

Lecture 22 Implementing Diagnostic Tools

Lecture 23 CHECKPOINT 7; Debugging

Lecture 24 CHECKPOINT 8; Implementing the SKPRM Strategy

Section 7: Portfolio Allocations with Strategy Signals

Lecture 25 Combining Alpha Signals For Portfolio Analysis

Lecture 26 CHECKPOINT 9; Controlling Nominal Exposure in a Vol Target Framework

Section 8: Integrating Order Logic with a Brokerage - Oanda

Lecture 27 Writing a Service Class API for Oanda

Lecture 28 Implementing the Service Class API and Creating an Order Config

Lecture 29 Getting Live Optimal Allocations and Integration with the Brokerage

Lecture 30 CHECKPOINT 10; Implementing Internal Order Logic and Utilities

Lecture 31 Completing Order Logic and Considerations for Other Brokerages

Section 9: Dual Brokerages - Integrating with Darwinex Platform

Lecture 32 Setting Up With Darwinex - MQL and Python Scripts

Lecture 33 Obtaining Data Through a TCP Socket Connection with an Open MT4 Terminal

Lecture 34 CHECKPOINT 11; Writing Client-Server Scripts In Python and MQL

Lecture 35 Scraping the Darwinex Website for Contracts

Lecture 36 CHECKPOINT 12; Writing the Darwinex Wrapper API and Configs

Lecture 37 Implementing the Darwinex Service Client

Lecture 38 Implementing the Darwinex Trade Client

Section 10: Multiple Brokerages and Contract Switching

Lecture 39 CHECKPOINT 13; Integrating Another Brokerage (Darwinex) with a Master Switch

Lecture 40 Getting The Darwinex Dataset

Lecture 41 CHECKPOINT 14; Integrating the Darwinex Data Pipeline

Lecture 42 Integrating Darwinex Strategy Configs

Section 11: Trade Order Submission and Obtaining Portfolio Allocations

Lecture 43 Market Order FOK - Oanda

Lecture 44 Data Cleaning and Rerunning Tests

Lecture 45 CHECKPOINT 15; End-to-End Testing of Order Logic and Concluding Oanda

Lecture 46 Writing the Trader Order Logic in Darwinex Trade Client

Lecture 47 Min Heap Data Structure for Open Trades

Lecture 48 Implementing the Darwinex Trade Order Logic - Smallest In First Out

Lecture 49 End to End Testing of Darwinex Trade Order Logic

Lecture 50 CHECKPOINT FINALE; Conclusion

This course is for traders and programmers looking to implement multi-strategy quantitative portfolios for research or trading purposes in non-HFT spaces.,For algorithmic traders who wish to have a more professional setup to integrate their strategies into more robust frameworks for their return harvesting.

Fikper

https://fikper.com/Mt2Z0kZ9NI/Udemy_Multi-Strategy_Quant_Systems_Algorithmic_Trading_in_Python.part1.rar.html

https://fikper.com/IIFRotaqfs/Udemy_Multi-Strategy_Quant_Systems_Algorithmic_Trading_in_Python.part2.rar.html

https://fikper.com/osamTtNTrb/Udemy_Multi-Strategy_Quant_Systems_Algorithmic_Trading_in_Python.part3.rar.html

FileAxa

https://fileaxa.com/jkh585pctp4t/Udemy_Multi-Strategy_Quant_Systems_Algorithmic_Trading_in_Python.part1.rar

https://fileaxa.com/mptu4yk7r4de/Udemy_Multi-Strategy_Quant_Systems_Algorithmic_Trading_in_Python.part2.rar

https://fileaxa.com/5jxk6dr4apf1/Udemy_Multi-Strategy_Quant_Systems_Algorithmic_Trading_in_Python.part3.rar

RapidGator

https://rapidgator.net/file/53e28ff7b9215adebe5e159afe12a17c/Udemy_Multi-Strategy_Quant_Systems_Algorithmic_Trading_in_Python.part1.rar

https://rapidgator.net/file/5448e3ba0d02b50b1b2d31534920b6f4/Udemy_Multi-Strategy_Quant_Systems_Algorithmic_Trading_in_Python.part2.rar

https://rapidgator.net/file/214b5fe8112f6e68257bf644e26a8e06/Udemy_Multi-Strategy_Quant_Systems_Algorithmic_Trading_in_Python.part3.rar

TurboBit

https://turbobit.net/w238hnecutta/Udemy_Multi-Strategy_Quant_Systems_Algorithmic_Trading_in_Python.part1.rar.html

https://turbobit.net/cga6rc5lc5hb/Udemy_Multi-Strategy_Quant_Systems_Algorithmic_Trading_in_Python.part2.rar.html

https://turbobit.net/ydcl7vgcdoqw/Udemy_Multi-Strategy_Quant_Systems_Algorithmic_Trading_in_Python.part3.rar.html